The cost-of-living crisis

Taking a more in-depth look at the impact of the costs of living, pragmatism has clearly been the name of the game. Shoppers learn something from every crisis and – much more than in stable times – share a collective mindset: The Cost-of-Living crisis propelled planning, frugality and focus.

More than one in three households feels budgetary restraints, though the number has dropped slightly compared to half a year ago. Also, country dynamics differ considerably: the number of households struggling reaches 50% or more in countries, including Spain and Hungary. In the latter, the situation is worsening, as it is in Sweden and Austria, though on a lower level. Countries with the highest share of comfortable shoppers include Denmark, Germany, the Netherlands, the Czech Republic and Poland – and on a positive note: the overall situation is improving or at the very least stable in the majority of countries.

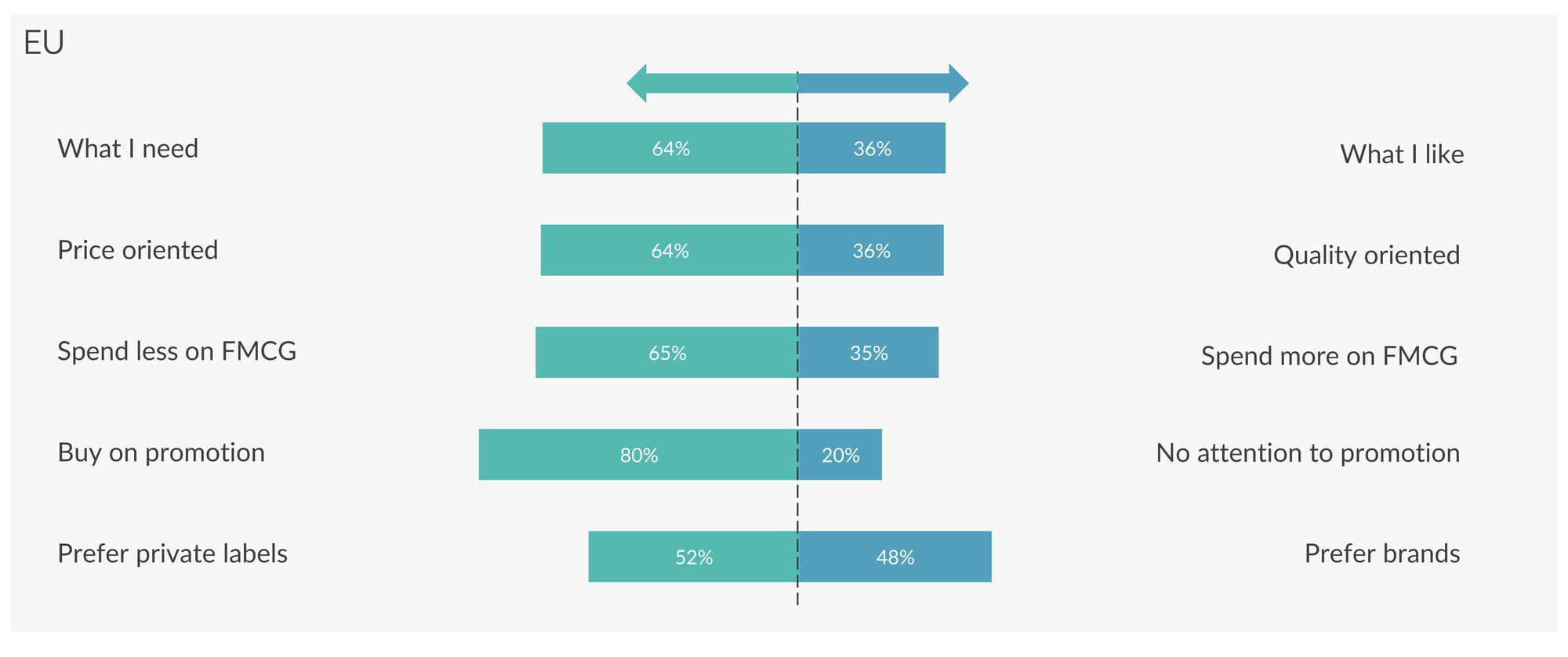

Across Europe, shoppers were nonetheless forced to develop a less for less mindset: buy what you need rather than what you like, focusing on price, planning to spend less, buying on promotion, with a slight preference for private labels.

Still 65% of shoppers plan to spend less on FMCG. Even though the budget situation seems to stabilize or improve slightly, the sustained high price levels and the overall uncertainty are leading shoppers to further intensify their pragmatic behavior.

Two in three shoppers declare to check prices (even) more than before, an increase compared to half a year ago. Almost all coping behaviors are increasing, especially the intention to cut down on food waste. However, buying more regional is bouncing back and also – though at the very bottom – the resolution to treat oneself a bit more, which could be a first sign of slight recovery: shoppers are planning to “revive” preferences and principles.

Two-thirds rather plan to spend less on FMCG

In fact, we are facing a polarized situation as the Cost-of Living crisis normalizes down-trade or leave what you do not need and spend on what you think is really worth it.

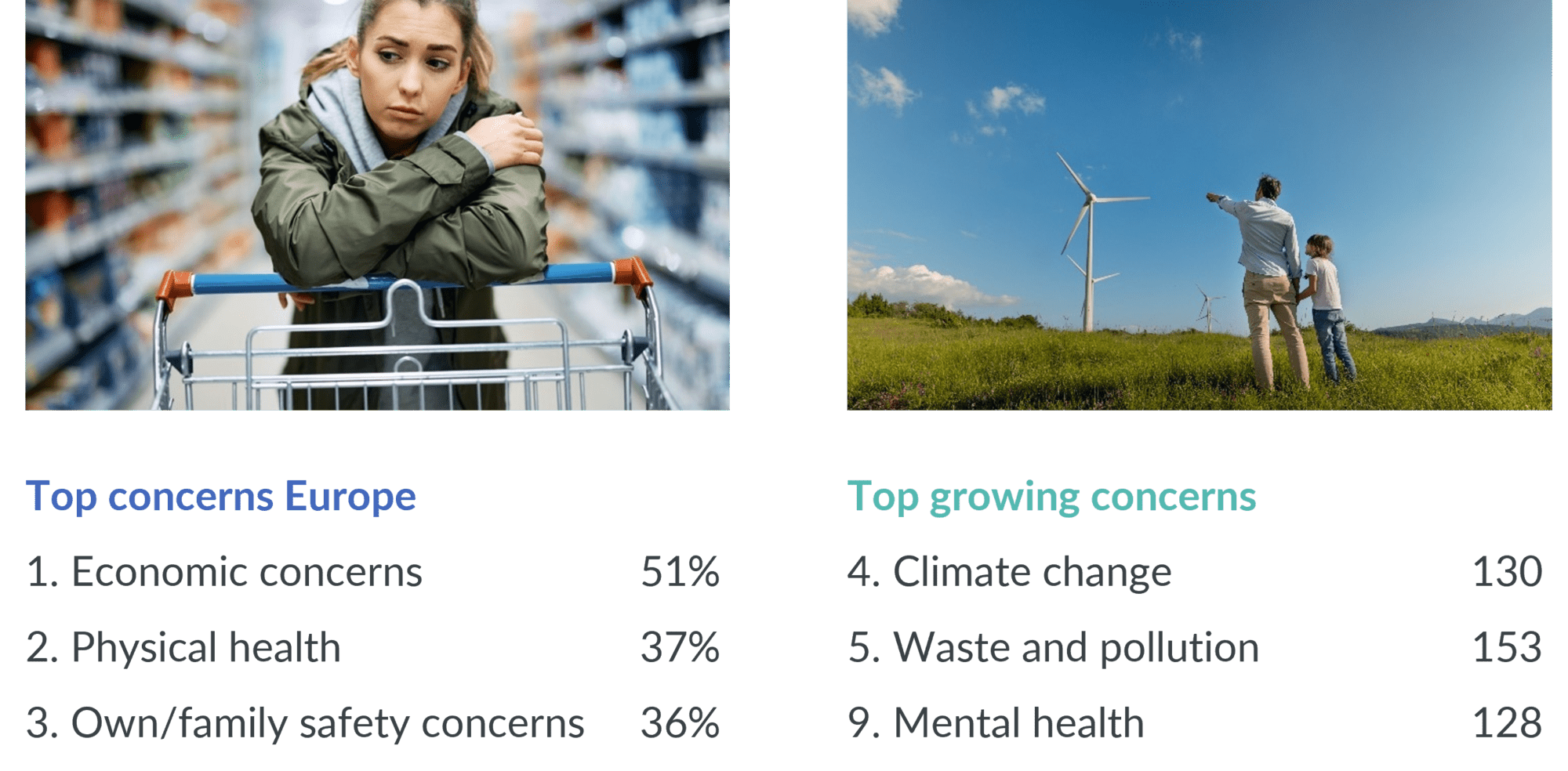

Budget certainly continues to be the primary concern across Europe. However, 2023 is seeing a tipping point, as the fastest growing concerns - after a glitch last year - are worries about the environment. Climate change, waste and pollution are back on the agenda. In Austria, Germany and Italy, climate change even outranks budget as the primary concern. As the crisis stretches on, mental health concerns are also growing, especially among younger generations.

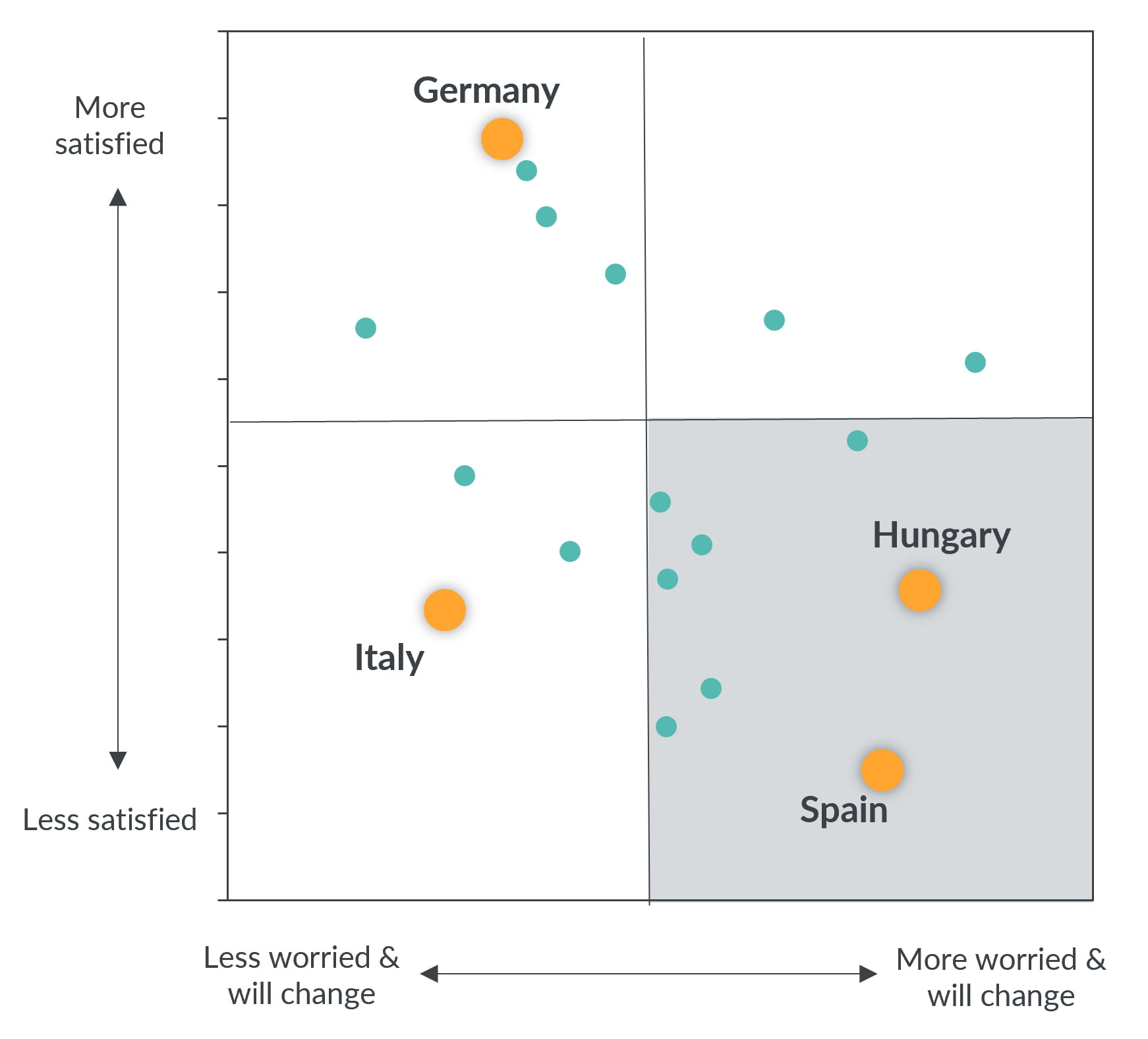

Nonetheless, the way out of the permacrisis will be a bumpy ride and there is surely not one speed for all, as a closer look at two premises for change reveals: 1 – the overall levels of satisfaction with the total FMCG offer, assuming that less satisfaction means more risk of change; and 2 – the inflation worries and the intention to change effect, with a few countries in a particularly difficult situation. Hungary and Spain are exemplary countries were worries and planned action are high, accompanied by high levels of dissatisfaction. By contrast, countries like Germany seem on a faster track to 'normalcy’.

It is interesting to observe how the coping strategies are evolving: At the beginning of the cost-of-living crisis, coping centered very much around buying less, on offer, or cheaper. These measures still count but to a lesser extent. They are now more often replaced by the ultimate coping mechanism of not buying any longer, provided the nature of the category allows it. This represents a real threat to volumes and a high chance of being left out of the basket. In categories where not buying is not really an option, we are seeing more stockpiling at the lowest price and buying elsewhere, i.e. shopping around for the best buy. This is a good example of the polarized basket situation: shoppers leave what they do not really need (or care for) and go to greater lengths to secure what they do not want to compromise on.

Obviously, some categories run a greater risk of further adaptive behaviors than others and three categories continue to be in the top 3 of a most likely change of behavior: the indulgence categories, the nice to haves, including alcohol and confectionery, and cosmetics. But there is a silver lining: compared to previous measurements, the situation for these categories is improving, as less shoppers have singled them out for further change. The attention is – sometimes forcefully – turning to daily necessities, such as fresh fruits and canned food.

Of course, adaptive behaviors also have an effect on retailer loyalty. During the pandemic, the predominant strategy was fast, one-stop-shopping. Now, we are seeing an uplift in shopping around and cherry-picking small baskets. On average, 19% of shoppers in Europe state that they plan to shop less or stop shopping at all at what they consider their main retailer. At 29%, these numbers are especially alarming in France and Sweden.

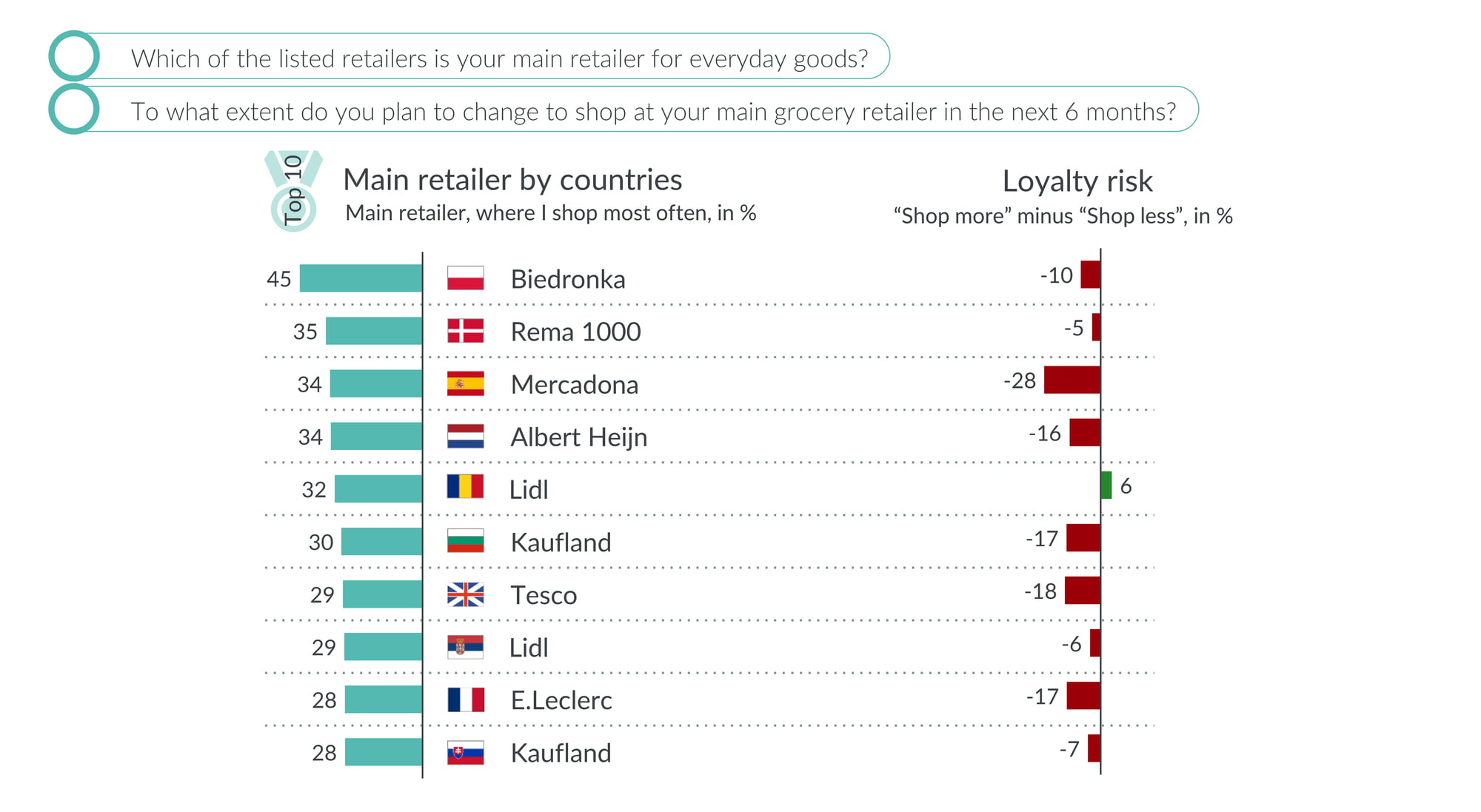

Looking at Europe’s most preferred retailers – those with the highest share of shoppers naming the respective retailer as their main one – some run a high risk of losing out, especially Mercadona in Spain, whereas Lidl, e.g. in Romania, has a more favorable profile.

Risks for retailers also bear risks for brands, as shoppers develop a certain inertia in their behavior. For example, the likelihood of a shopper buying a large brand again increases from 40% at the second purchase, to 60% at the third one. But this likelihood is easily cut in half when shoppers switch retailers.

Mercadona has highest risk; Lidl more favorable

So, the very first order of business in moving past the permacrisis: make it easy to be bought. As many categories are left out of the basket, it means familiarizing shoppers with the category, led by consumption occasions. And it means, be where the shopper is and invest heavily in conspicuity, i.e. be visible on the shelf.