In times of budget squeezes and intensified rational buying decisions, it is extremely important to get your message across and differentiate through product benefits. Hence there is a need to understand what is important to shoppers, besides the cost-of-living-crisis.

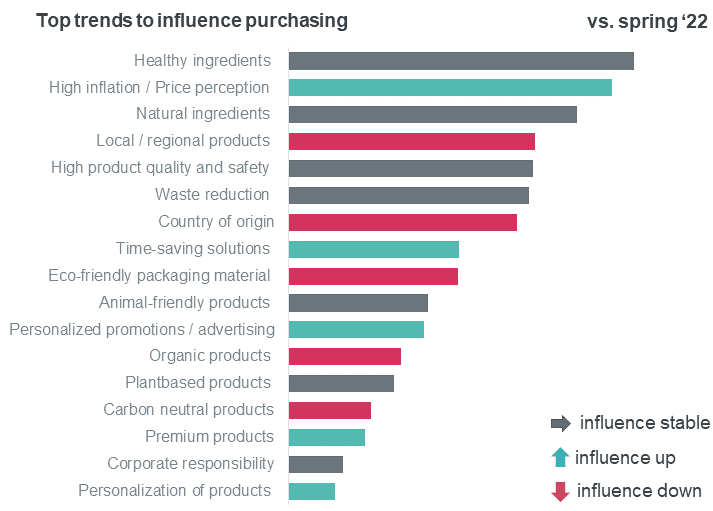

Not surprisingly, inflation and (perceived) high prices moved up the list of factors influencing buying decisions, currently at no. 2. But healthy and natural ingredients continue to rank in first and third place among the choice factors, whereas local and regional have lost a bit of momentum. Compared to spring this year, personalization has considerably gained in relevance. This is particularly the case for promotions, as shoppers try to make their limited budgets meet their needs. Time-saving solutions are also rising in demand - and in spite of overall down-trading there is a small but growing window for premium products.

Health-focus proves to be crisis-resistant. However, healthy living and healthy ingredients have noticeably changed their meaning and are becoming more particular. Free of artificial ingredients, low on sugar and not genetically modified are still important to at least 1 in 3 shoppers, but micro-level nutrients and particular lifestyles or diets are gaining ground. This includes aspects such as rich in protein and free of lactose or gluten as well as veganism and diabetes. On average, 11% of European households have at least one person needing to watch their diabetes, 9% have a least one person being intolerant to lactose, and 4% count at least one vegan in the household.

Naturally healthy still important influencer

In the current cost-of-living-crisis it is essential to permanently monitor and adapt to changes in shopping behavior. At the same time, it is important to not lose sight of long-term macrotrends. This whitepaper focuses specifically on the impact of the current inflation and instability, with predictions on the next six to twelve months. Strategy and tactics need to embrace these short-term trends while long-term perspectives should not be deprioritized, in order to pave the way out of the perma-crisis. For the sake of perspective, this paper is zooming in on e-grocery, which (only) has a 6% share in FMCG in Western Europe1. Eco-actives currently account for a 26% share in FMCG and the long-term business potential of eco-consciousness will persist. Although we currently observe a deceleration in green trends, we are expecting this to be a glitch.

Similarly, European countries are showing different trend patterns that require different strategies. For example, carbon-neutral is an important long-term trend for 21% of German consumers, but only for 10% of Polish shoppers.

In general, financially comfortable shoppers continue to show a stable preference for premium products as well as aspects including organic, carbon neutral and corporate responsibility, while for struggling consumers healthy, time-saving and personalized promotions are stronger influencers of buying decisions at present.

Personalized promotions will certainly not be a short-term fad. Online leaflets and digital loyalty schemes are continuously expanding their reach across Europe and the regular use of online leaflets has increased by 6%.

1 Six biggest countries in Western Europe