Fine spirits and wine, gourmet food, special offerings for vegan and allergic consumers, but by no means a mass market for daily grocery shopping. Due to the pandemic and numerous lockdowns in European countries, shopping behavior has changed dramatically over the past months.

This white paper explores the recent developments of E-Commerce in FMCG in Europe with a primary focus on the retail perspective, comparing regional differences, and also adding the global view. Interviews with GfK experts provide additional insights into country specifics and complement the outlook on E-Commerce trends in FMCG that might be here to stay.

Part 1 of this paper takes a look back at 2019 and the pre-COVID situation, Part 2 analyzes the development of E-Commerce during the first lockdowns until May 2020, also adding findings until September 2020. A full report on the national development of E-Commerce in 15 European countries has been available since December 2020.

For our study we analyzed data from the GfK Consumer Panels, which collect high-quality data from households, who record their daily purchases with a barcode hand scanner or smartphone. Our partner Kantar provided additional regional support.

Learn more about country specifics from GfK experts, who contributed to this white paper:

Norman Buysse - Director Retail, GfK Netherlands

Marco Pellizzoni - Commercial Director Consumer Panel, GfK Italy

Dr. Benjamin Brinkhoff - Account Director, GfK Germany

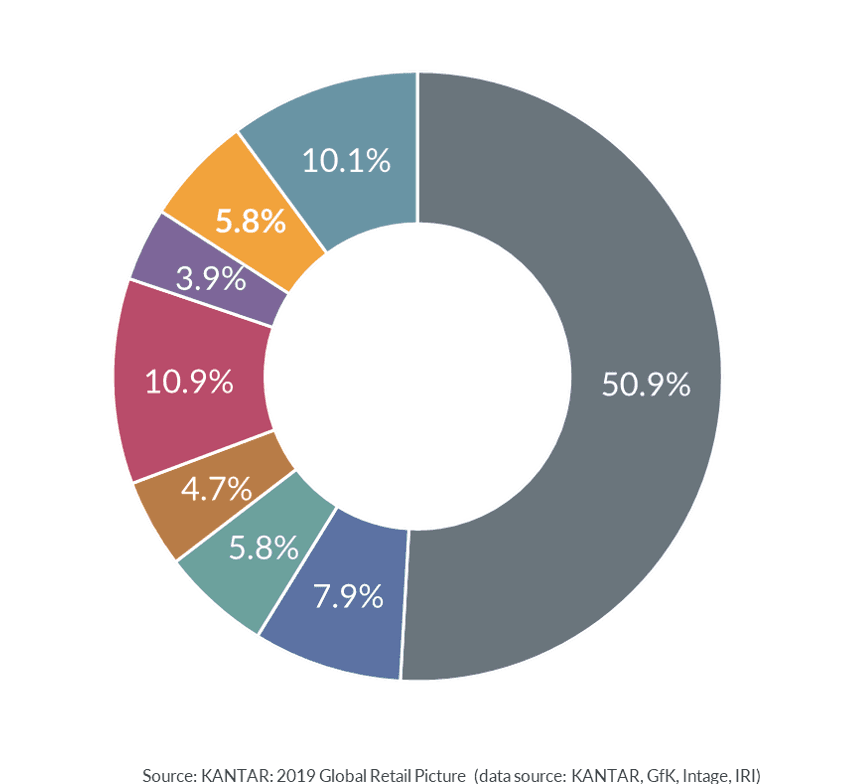

Until 2019, E-Commerce in FMCG was a fairly small channel segment, even on a global scale. With a value share of 5.8% it was on par with Drugstores and Pharmacies, only beating Cash & Carry markets and Convenience Stores.

Even traditional Grocery Stores achieved a value share of 7.5%, with Hypermarkets and Supermarkets in the lead – by far, with as much as 50.9%.

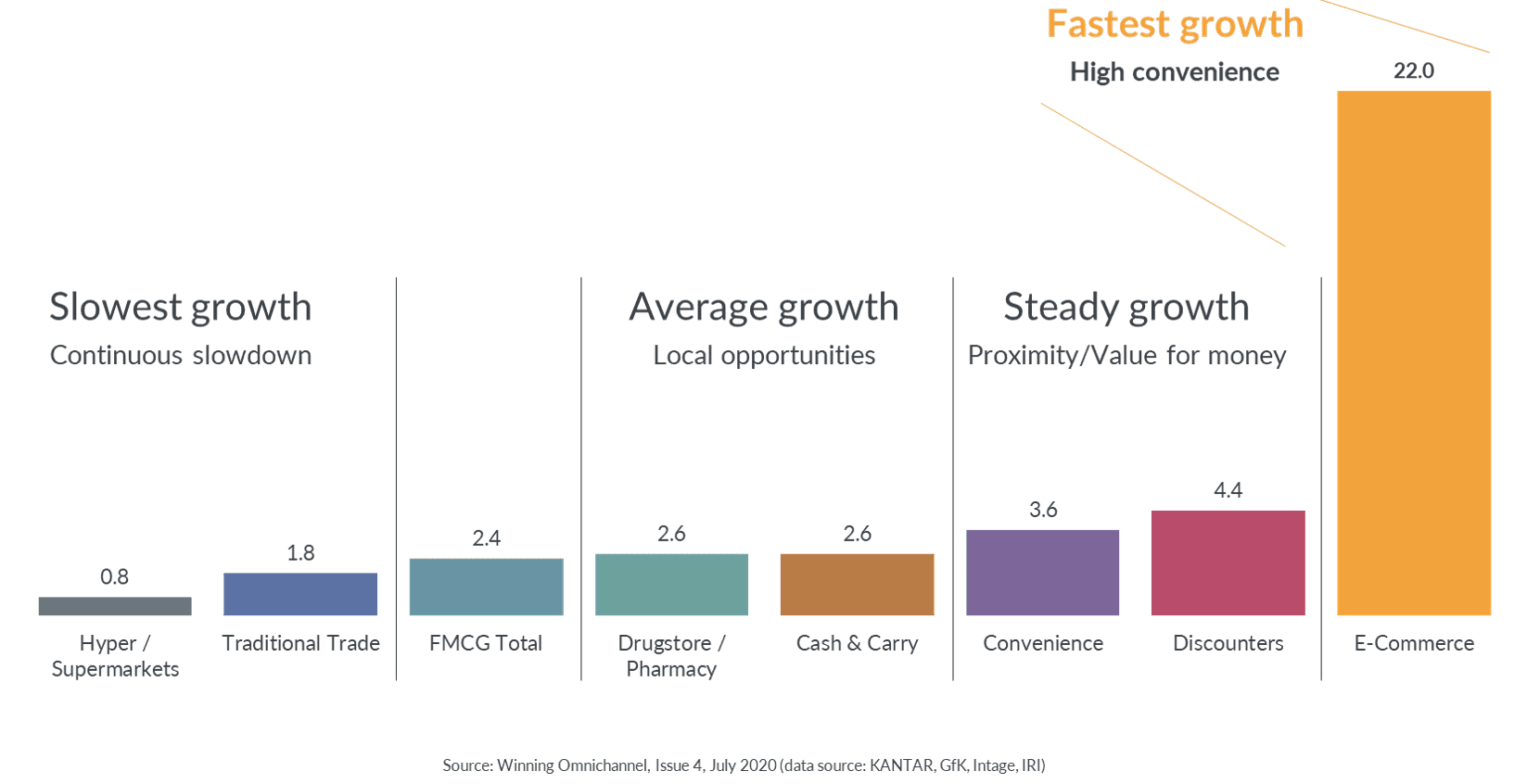

However, looking at growth rates shows a different picture and a lot of potential: Compared to 2018, E-Commerce experienced the highest and the only double-digit growth rate, reaching +22% in 2019, while total value growth of the FMCG market amounted to +2.4%. On the low end of the scale: Hypermarkets and Supermarkets as well as traditional Grocery Stores experiencing a continuous slowdown with merely +0.8% of value growth and +1.8%, respectively.

Global FMCG value growth in % - 2019 vs. 2018

Discounters generated the second largest growth rate with +4.4%, and Convenience Stores achieved +3.6%, both winning on proximity and value for money, whereas the key argument in favor of E-Commerce is clearly the high convenience of the channel.

The following number indicates the direction the market is going: Already in 2019, E-Commerce contributed 45% to the global growth in FMCG, followed by Discounters (20%), and Hyper- and Supermarkets (18%).

Channel contribution to FMCG growth in % - 2019

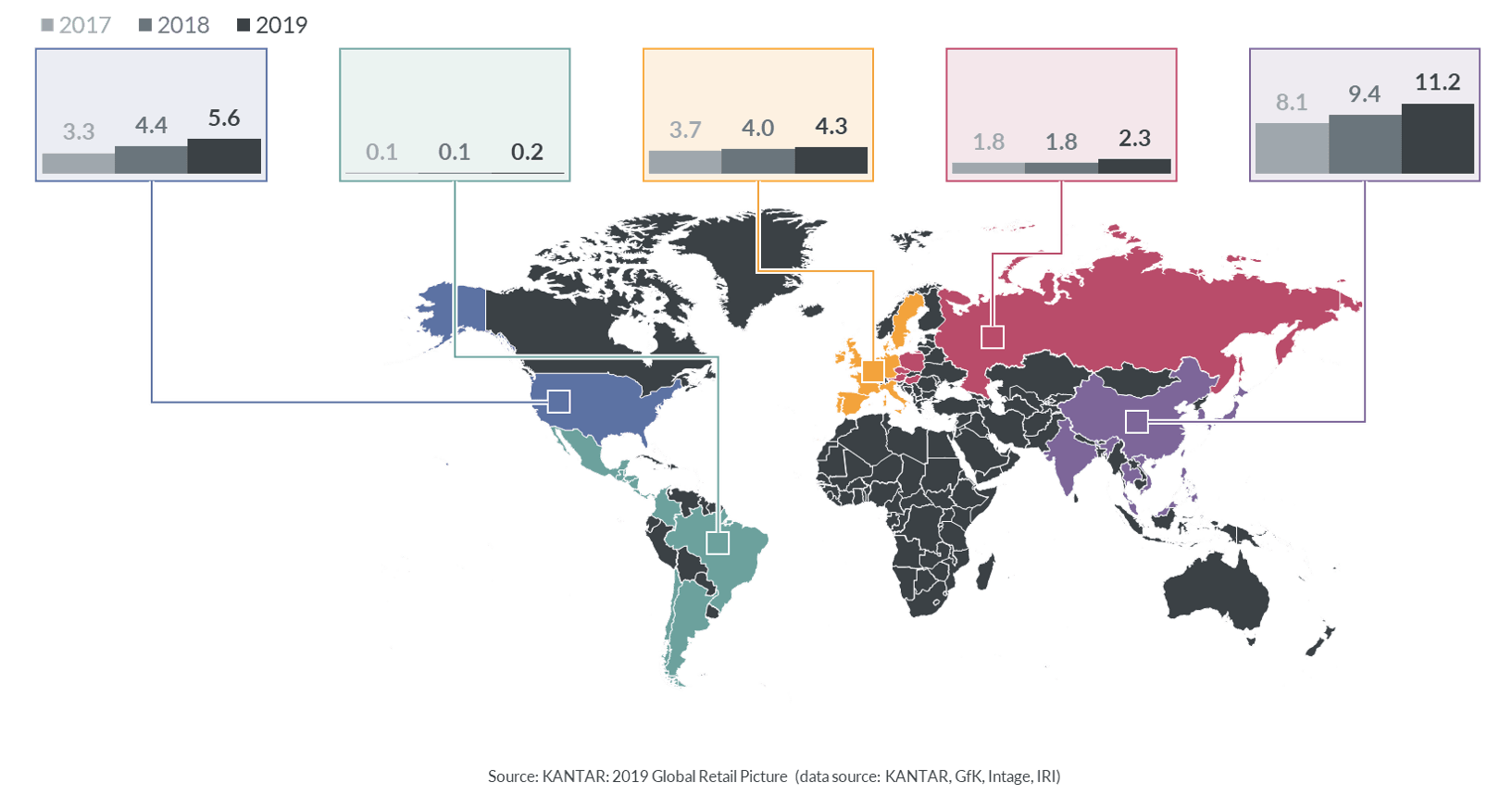

The analysis of E-Commerce value shares on a regional level displays a very disparate market situation for this channel: While doubling its value share, E-Commerce in Latin America only rose from 0.1% in 2017 to 0.2% in 2019. In Central and Eastern Europe, the E-Commerce share remained static at 1.8% in 2017 and 2018, increasing to 2.3% in 2019.

Compared to the US (3.3%), the Western European region saw a higher value share at 3.7% in 2017, falling behind in 2018 with 4.0% and 4.3% in 2019. For the same period, the USA reported an increase to 4.4% and then 5.6% for 2019, making it the number two region in value share globally. However, this is still only half of the value share that E-Commerce generated in Asia, where it rose from 8.1% in 2017 to 11.2% in 2019.

E-Commerce value share in %

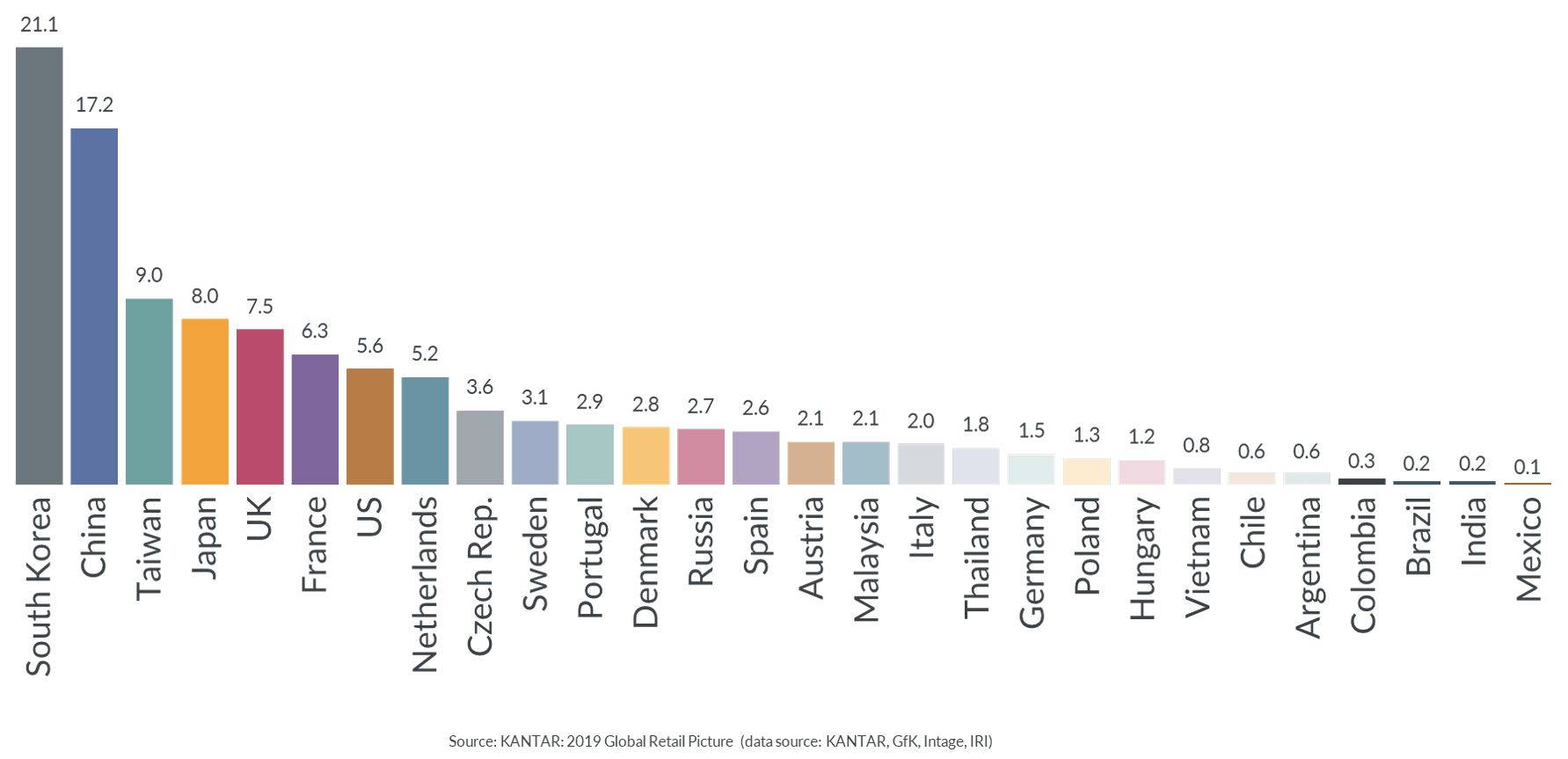

A closer look at individual countries displays high discrepancies in value share. It can come as no surprise that the four leading countries are based in Asia: South Korea leads the E-Commerce way with 21.1%, followed by China at 17.2%, Taiwan (9%) and Japan (8%). Ranks 5 and 6 go to the UK (7.5%) and France (6.3%), followed by the US and the Netherlands (5.2%), whereas Germany is listed 19th – of 28 countries – with a value share of 1.5% for 2019.

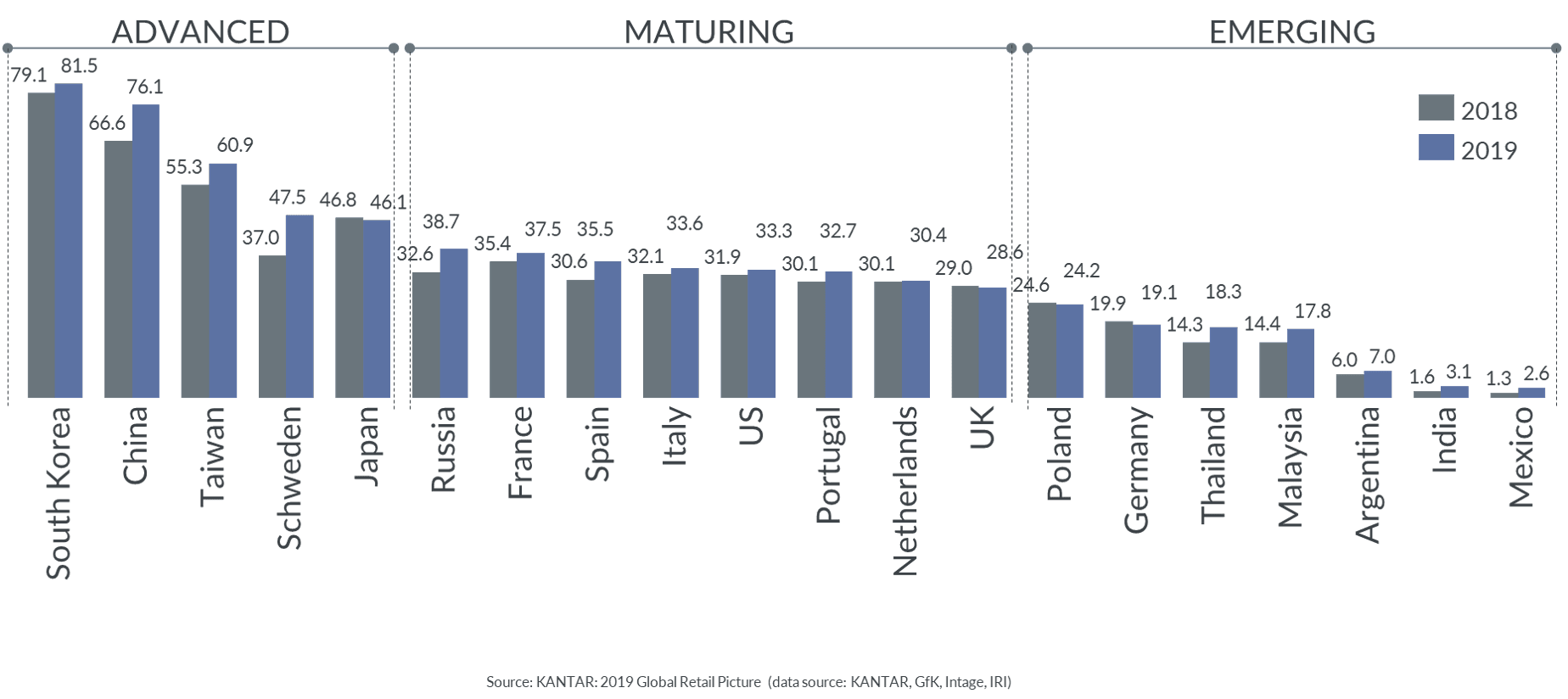

When it comes to channel penetration, South Korea again sets the benchmark with 81.5% in 2019. But Chinese shoppers are catching up and the penetration jumped by nearly 10 percentage points to 76.1% last year. Again, four out of five of the most advanced E-Commerce markets with a high penetration above 40% are to be found in Asia, with only the technology-savvy shoppers in Sweden reaching this elite group. In Sweden, E-Commerce penetration soared from 37% (2018) to 47.5%, overtaking Japan, which declined slightly to 46.1% in 2019 (from 46.8%).

Talking about a decline in channel penetration, Germany lists among those four countries having experienced a decrease for 2019, from 19.9% to 19.1%. Apart from Japan and Germany, this group includes Poland – with a penetration of 24.2% – and the UK at 28.6%.

Loyalty of E-Commerce shoppers in %

E-Commerce penetration in %

Penetration is key for the long-term success of FMCG in E-Commerce. Once shoppers have ventured into this channel, they tend to be fairly loyal. When it comes to shopper loyalty, Europe still has a long way to go, compared to Asian countries. Advanced markets such as South Korea, Japan, Taiwan and China observe a loyalty of E-Commerce shoppers between 25% and 39%, with only the UK coming close: Here, consumer loyalty reaches 23%, ranking highest in Europe. France, Denmark and the Netherlands still achieve double-digit loyalty rates between 17% and 13%, whereas Germany and Spain show fairly low rates at 7%, nearly on par with Russia (6%).

Value share in % - 2019

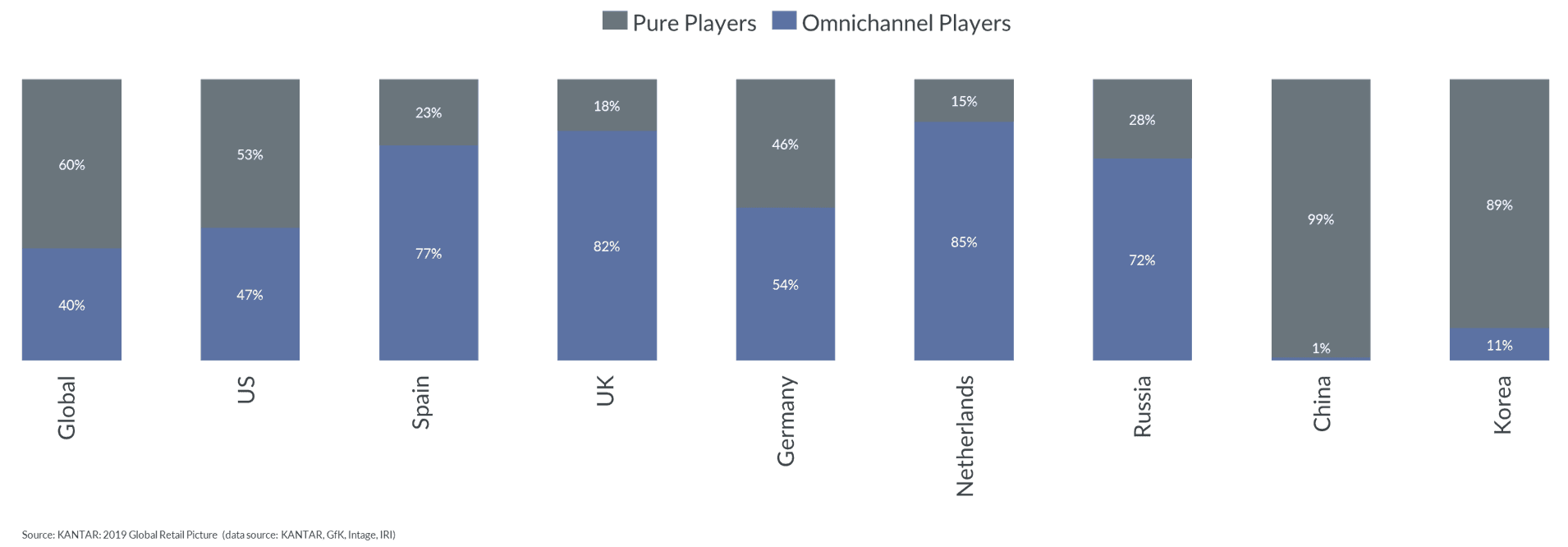

No market is the same. Looking at the players in the arena of E-Commerce in FMCG, every country has a different composition.

Globally, 40% of E-Commerce market players are omnichannel retailers, 60% pure play online retailers. But this global average is misleading because the regions differ considerably.

Looking at Asia, namely China and South Korea, E-Commerce in FMCG is dominated by pure players, such as Alibaba, Meituan or Pinduoduo in China. In Germany and the US one can find a more or less even mix of pure and omnichannel players, whereas in other European countries more than two thirds of the FMCG retailers also offer E-Commerce to complement their stationary presence.

So, there is no one formula for success, especially none that could be replicated across different countries. Each market has its own characteristics, shoppers’ preferences, traditions and habits. As a result, the E-Commerce in FMCG venture requires a thorough analysis of local market conditions, shopper expectations as well as local challenges such as logistics, for example.

And the past months illustrate how market conditions can change very fast – this time in favor of E-Commerce in FMCG. In the following, we will take a closer look at the impact of COVID-19 on E-Commerce in Europe.