3. Consumption Driver

As inflation shifts, will volume lift?

In this chapter:

Assessing the economic divide

2025 spending intentions

Future growth expectations

Inflation has decelerated in many parts of the world. But the compounding effect of the past couple years will be felt for some time.

As consumers are balancing many competing life priorities, they may be driven to consume less in some spending categories—even if they have more funds to work with.

Gauging drivers of these tough choices is key to growing both sales and volumetric performance in 2025 and beyond.

Carman Allison

Vice President of Thought Leadership, North America, NIQ

“While consumers open their wallets and become less guarded with their spending going forward, the compounding effect of price increases means they're still spending 17% more than they were for the same goods in 2022. As we head into 2025, large brands will need to work hard to preserve their market penetration. Challenger brands in several categories are doing a better job of targeting consumer needs and are eroding brand loyalty. It’s important to understand the unique needs of your consumer segments to unlock growth.”

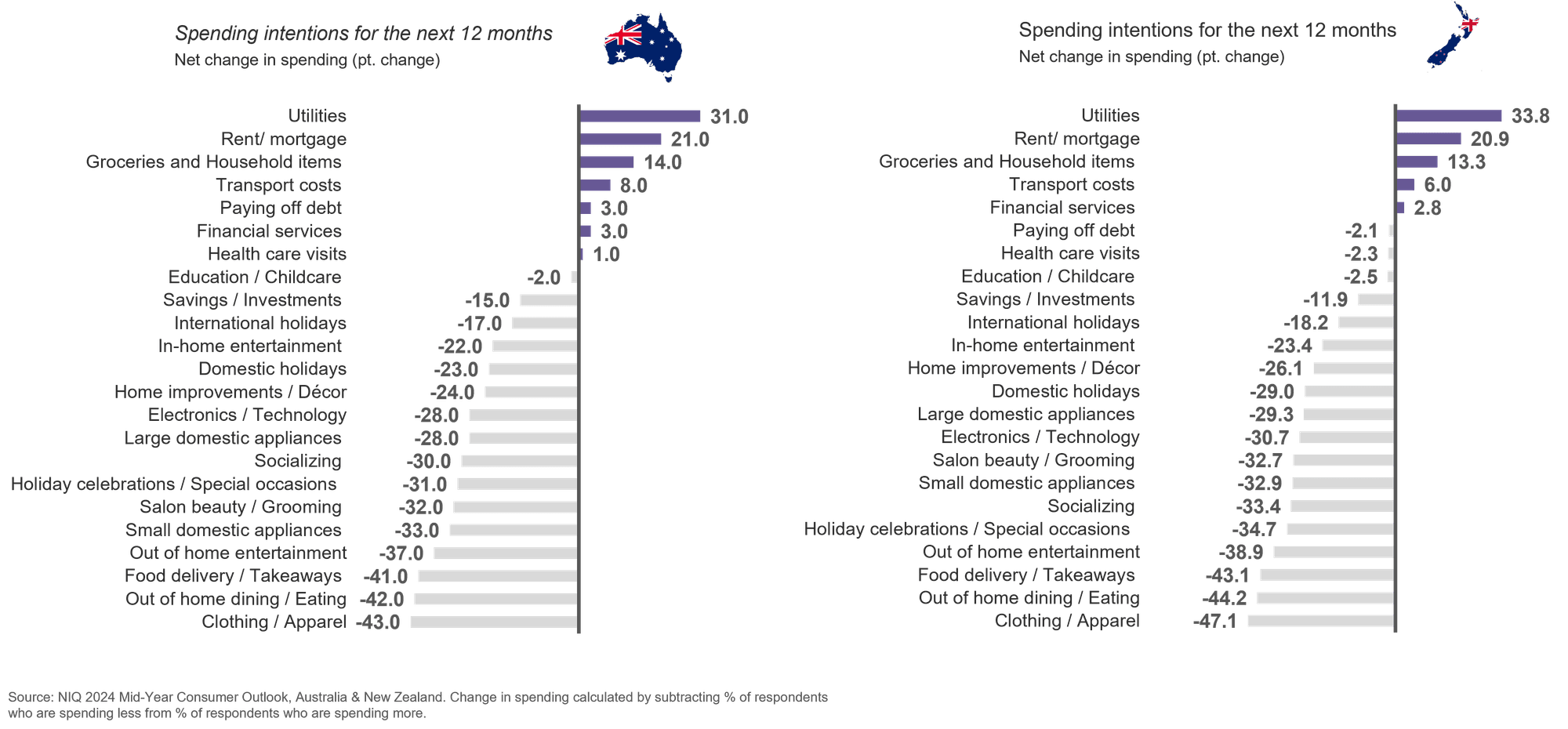

When consumers in Australia and New Zealand were asked about their spending expectations for the next 12 months, a clear pattern of rationalisation emerged. Many consumers anticipate increased spending on essential categories like utilities, housing, groceries, and transportation. Conversely, they plan to reduce spending on non-essential items and experiences, including clothing, dining out, takeaways, entertainment, and appliances. This mirrors a global trend where consumers are prioritising essential expenditures, such as rent/mortgage and healthcare visits, in the face of economic uncertainty and higher living costs.

It's important to acknowledge that many consumers still face financial constraints and are carefully balancing their budgets. The data also highlights the significant impact of "fixed costs"—essential expenses like utilities, rent, and healthcare—on consumer budgets. These non-negotiable costs limit discretionary spending even when the economic outlook shows signs of improvement. Consumers are re-allocating any financial gains towards these essential expenses, resulting in a relatively stable year-over-year trend in spending intentions.

Many discretionary categories show a propensity towards reduced spending, but a year-over-year comparison reveals a subtle shift towards greater optimism. Several categories, including dining out and alcoholic beverages, show less negative net change scores compared to mid-2023. Our of home dining saw a net change score of -26.7 in mid-2023, where today stands at -19.1. Similarly, within the CPG realm, while Alcoholic Beverages saw a score of -22.3 in mid-2023, that stands at -20.3 today, suggesting a potential, gradual return to discretionary spending.

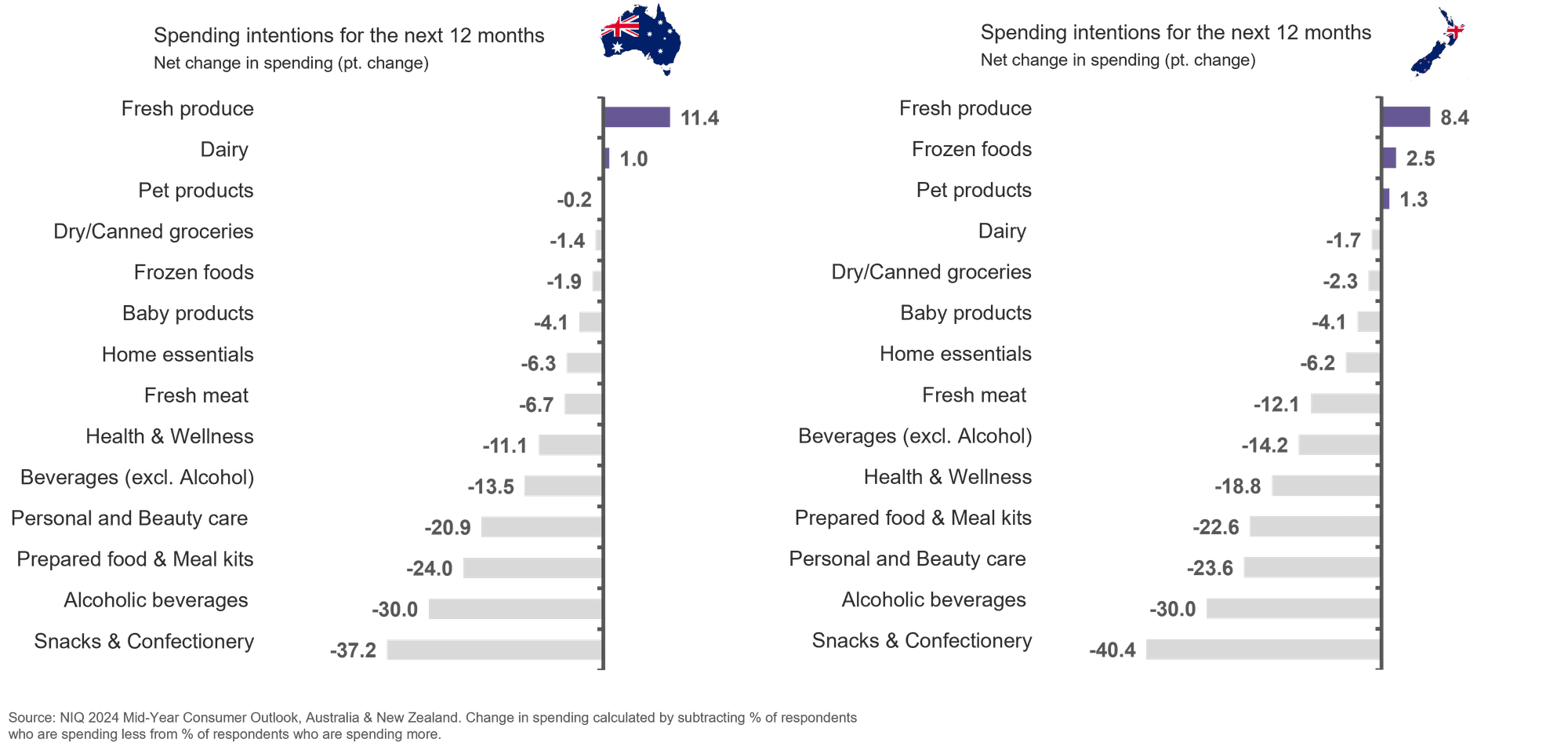

Consumer spending intentions in Australia and New Zealand reveal a clear trend towards rationalisation, with increased focus on essential grocery categories such as fresh produce, and decreased spending on discretionary items like snacks, confectionery, and alcoholic beverages. This prioritisation of essential grocery items aligns with broader consumer trends observed in overall spending habits. However, it's crucial to recognise that stated intentions don't always translate directly into actual behaviour. In the following sections, we'll delve into the actual performance of these grocery categories to understand how consumer actions align with their stated intentions.

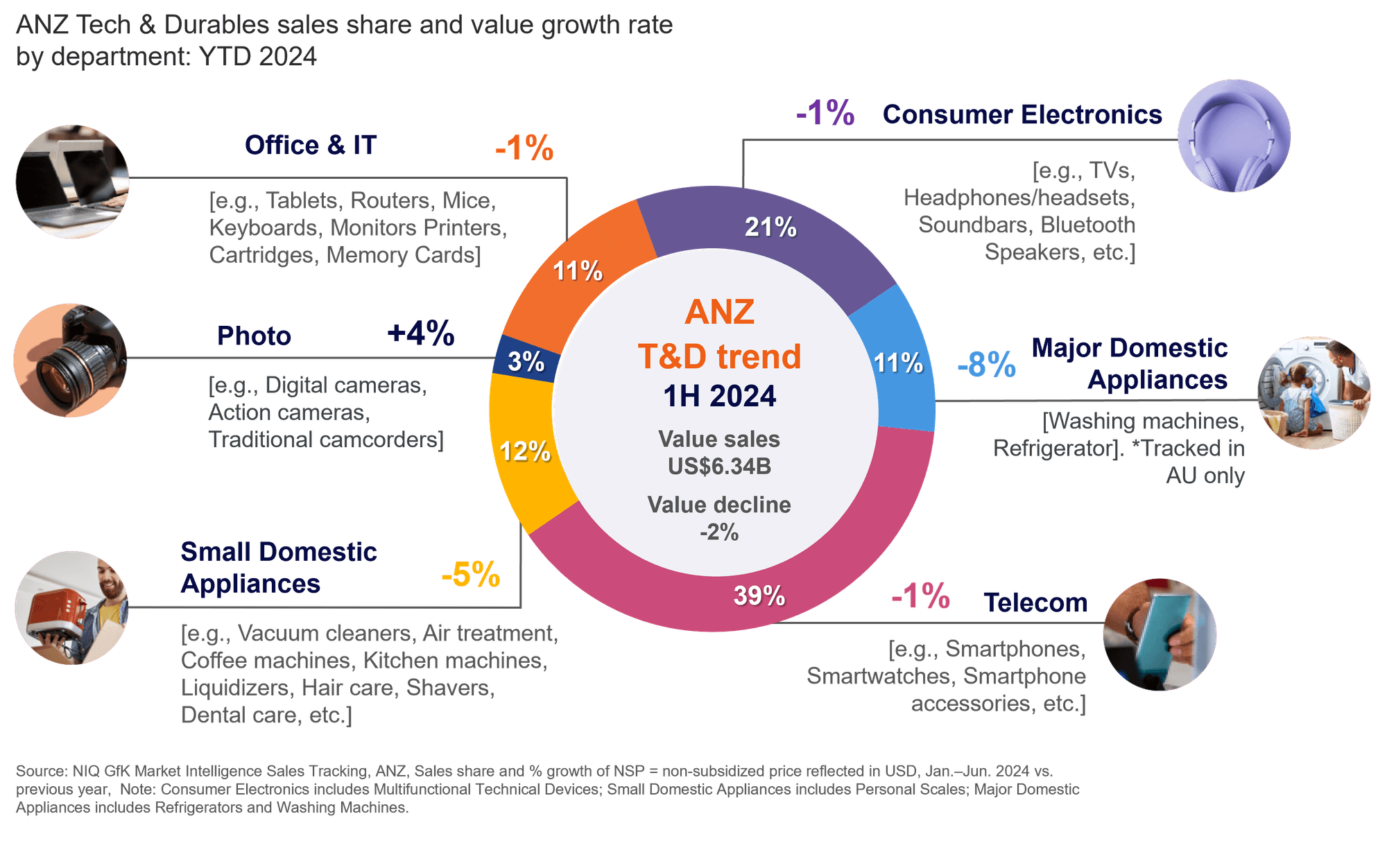

In the Tech & Durables sector, consumer actions are aligning with their stated intentions to reduce spending on non-essential items. The overall Tech & Durables market in Australia and New Zealand is experiencing a decline in value sales, primarily driven by reduced spending on domestic appliances.

Telecom, however, displays greater resilience, with a smaller decline attributed to the rising popularity of contract phones and the shift towards higher-quality mid-tier phones over flagship brands. Photo is the only segment experiencing growth, fueled by high-end cameras and lenses, although this growth is from a smaller base and does not offset the overall downward trend in the sector.

Several key factors are shaping the performance of specific categories within Tech & Durables:

IT: Larger-screen tablets (11"+) are driving growth in the IT sector.

Photo: The growth in this category is attributed to high-end cameras and lenses, as the low-end market is increasingly dominated by smartphones.

Major Domestic Appliances: Both washing machines and refrigerators are experiencing declines, with the latter seeing a shift in preference towards French door models over traditional top and bottom mount fridges.

These trends highlight the dynamic nature of the Tech & Durables market in Australia and New Zealand. While consumer intentions provide valuable insights, understanding actual market performance requires a deeper dive into the factors influencing specific categories and segments.

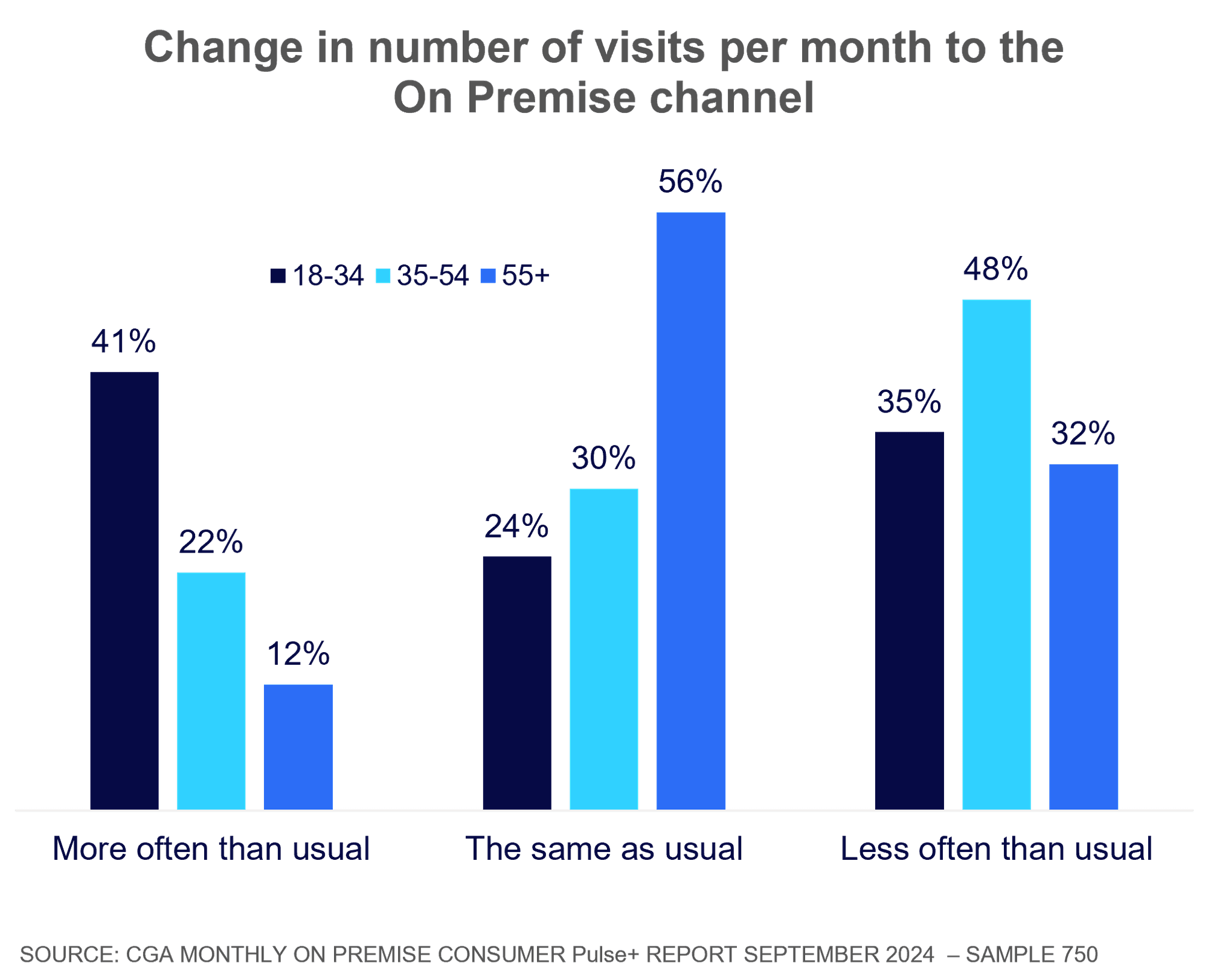

While the rising cost of living has led many consumers to reduce their spending on out-of-home entertainment, including visits to on-premise establishments, this trend is not uniform across all demographics. Contrary to expectations, middle-aged consumers (35-54) are more likely to reduce their on-premise visits compared to younger consumers (18-34). This may be attributed to the financial pressures faced by this age group, who often juggle expenses related to raising families and paying mortgages. Younger consumers, on the other hand, exhibit a more polarised behaviour, with a significant proportion (41%) actually increasing their on-premise visits.

This shift in on-premise consumption patterns has implications for beverage alcohol performance. While spirits have experienced significant declines in key markets like New South Wales and Victoria, beer has demonstrated greater resilience across all states. This can be attributed to beer's value proposition, as it is often perceived as a more affordable option compared to other alcoholic beverages.

Beer stands out as a value-for-money (VFM) option for consumers in New South Wales and Victoria, potentially influenced by higher housing costs in these regions.

As inflationary pressures gradually ease, concerns about everyday bills are diminishing, replaced by a greater focus on personal well-being, happiness, and job security. This shift reflects a growing sense of determination among consumers as they navigate economic uncertainties and make deliberate spending choices heading into 2025.

Total Beer Vol % chg vs YA: +3.3%

Total Spirits Vol % chg: +1.5%

Total Beer Vol % chg vs YA: -5.8%

Total Spirits Vol % chg: -8.9%

Total Beer Vol % chg vs YA: -2.9%

Total Spirits Vol % chg: -0.3%

Total Beer Vol % chg vs YA: +2.1%

Total Spirits Vol % chg: -15.7%

Total Beer Vol % chg vs YA: +5.4%

Total Spirits Vol % chg: -12.2%

On Premise sales performance L52 weeks

Share of total On Premise occasions vs YA

Events & special

occasions

+6pp

vs YA

Food-led

-4pp

Drink-led

-2pp

In a landscape where consumers are generally reducing their outings to save money, on-premise visits are increasingly focused on experiences. Events and special occasions now represent almost 40% of on-premise visits, a notable increase year-over-year. This highlights a shift in consumer behaviour, where on-premise visits are becoming less frequent but more deliberate and focused on meaningful experiences.

And here we have a few examples of the top occasions gaining most share within on-premise visits – a lot is related to sports and special occasions such as birthdays.

Top 4 occasions gaining most share vs YA

To watch live sport on television

Before/during/after watching live sport in a stadium

Special occasion (e.g. birthday, anniversary)

Themed event

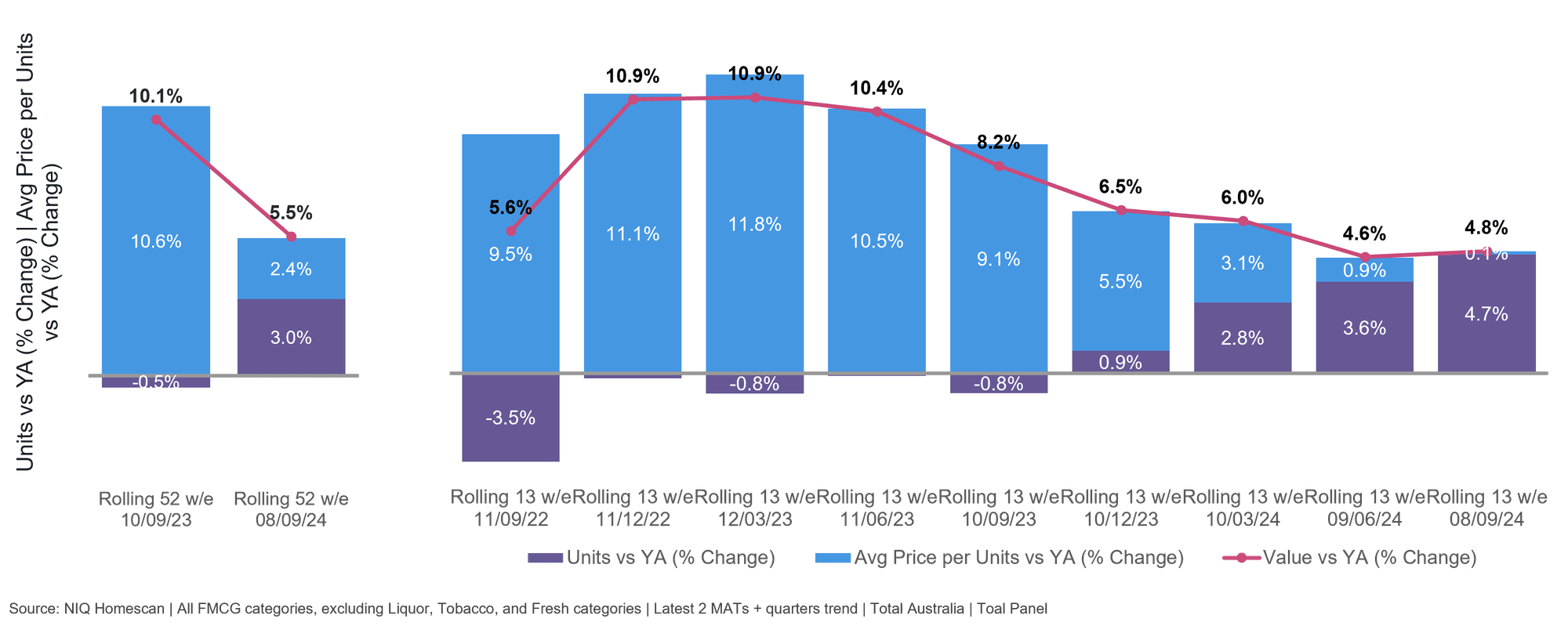

In the Australian FMCG market, value sales growth has been primarily driven by price increases since early 2022, reflecting a broader trend of high inflation. However, recent data indicates a positive shift. The growth of price-per-unit is decelerating, leading to a recovery in unit sales. This suggests that the market is moving towards a more volume-driven growth model, which is good news for the FMCG sector.

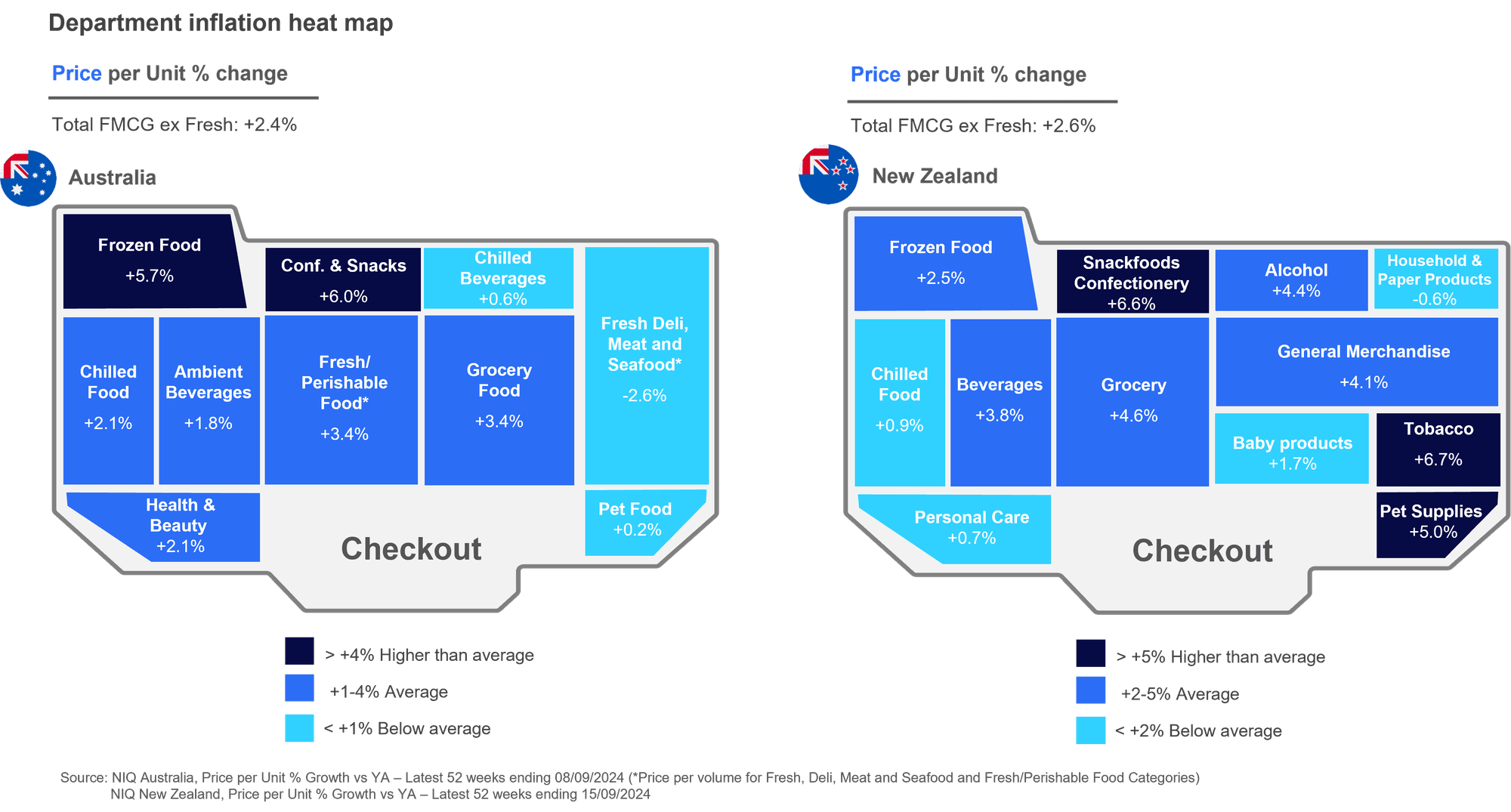

As global inflation decelerates, it's essential to identify the grocery categories where price increases are still prevalent. The provided heat map reveals that confectionery and snacks are among the most affected categories, likely due to the rising cost of cocoa. Conversely, fresh deli, meat, and seafood in Australia, and personal care/household items in New Zealand show lower price growth.

In these instances, growth is likely still going to be supported by higher prices, meaning companies operating in these categories should consider the limited purchasing power consumers continue to feel when buying these items regularly. In some categories such as Frozen Food, Perishables, and Health Care, consumers are already seeing prices ease quite a bit. Thus, companies with products in these areas will need to think of ways to sustainably push higher volumes of product without overpromoting, undervaluing or over-subsidising their offerings.

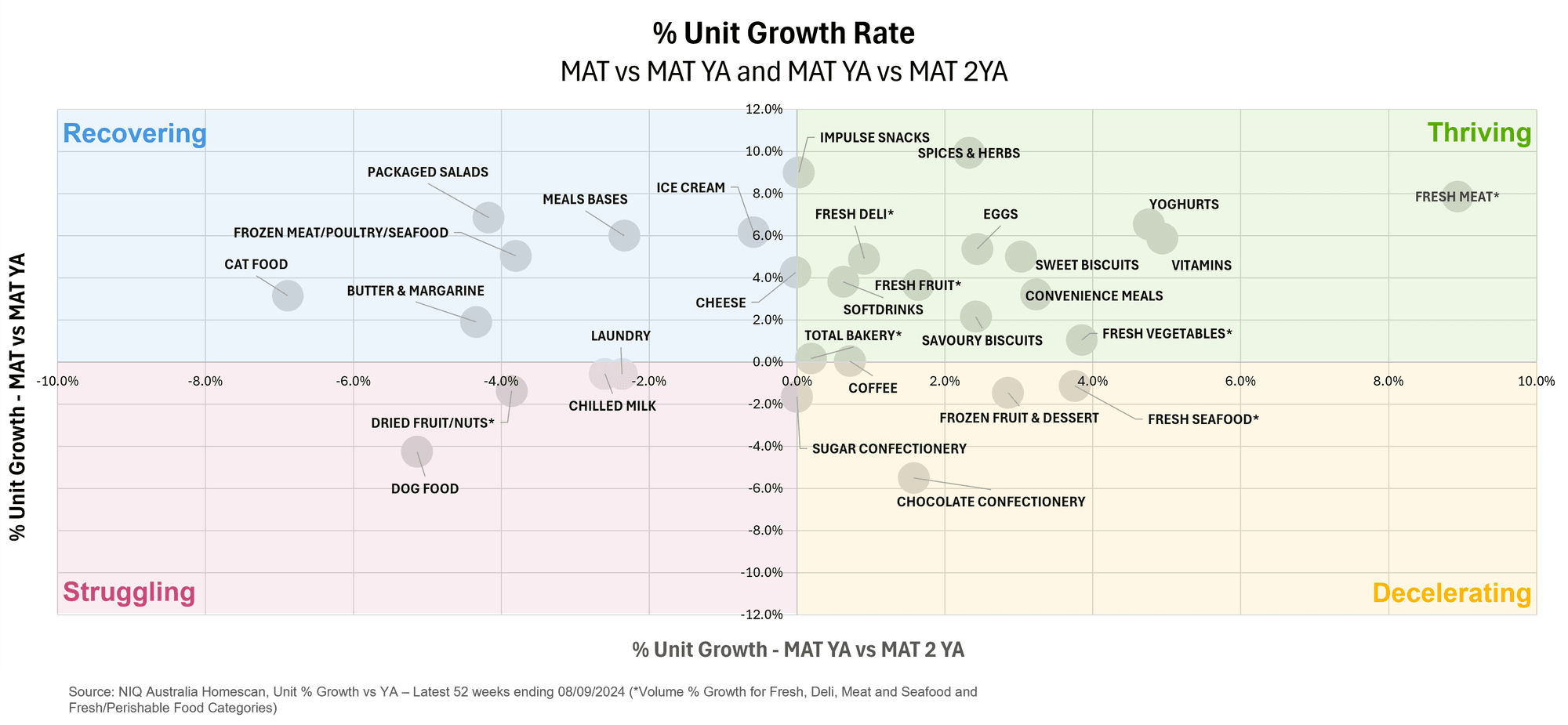

To understand the factors contributing to the recent unit growth and rebound in the Australian FMCG market, it's important to examine category-level performance over the past two years. By comparing year-on-year growth across different categories, we can identify those that are thriving, recovering, or decelerating.

Analysis reveals a significant contribution from food categories, particularly those related to in-home eating, among the categories that are thriving (consecutive growth in both years) and recovering (growth after a previous decline). This suggests a continued consumer preference for home-cooked meals, likely influenced by the ongoing cost of living pressures and a desire to save money.

On the other hand, chocolate confectionery shows a clear deceleration, primarily driven by higher prices. This highlights the sensitivity of consumers to price increases in discretionary categories, particularly those impacted by rising commodity costs.

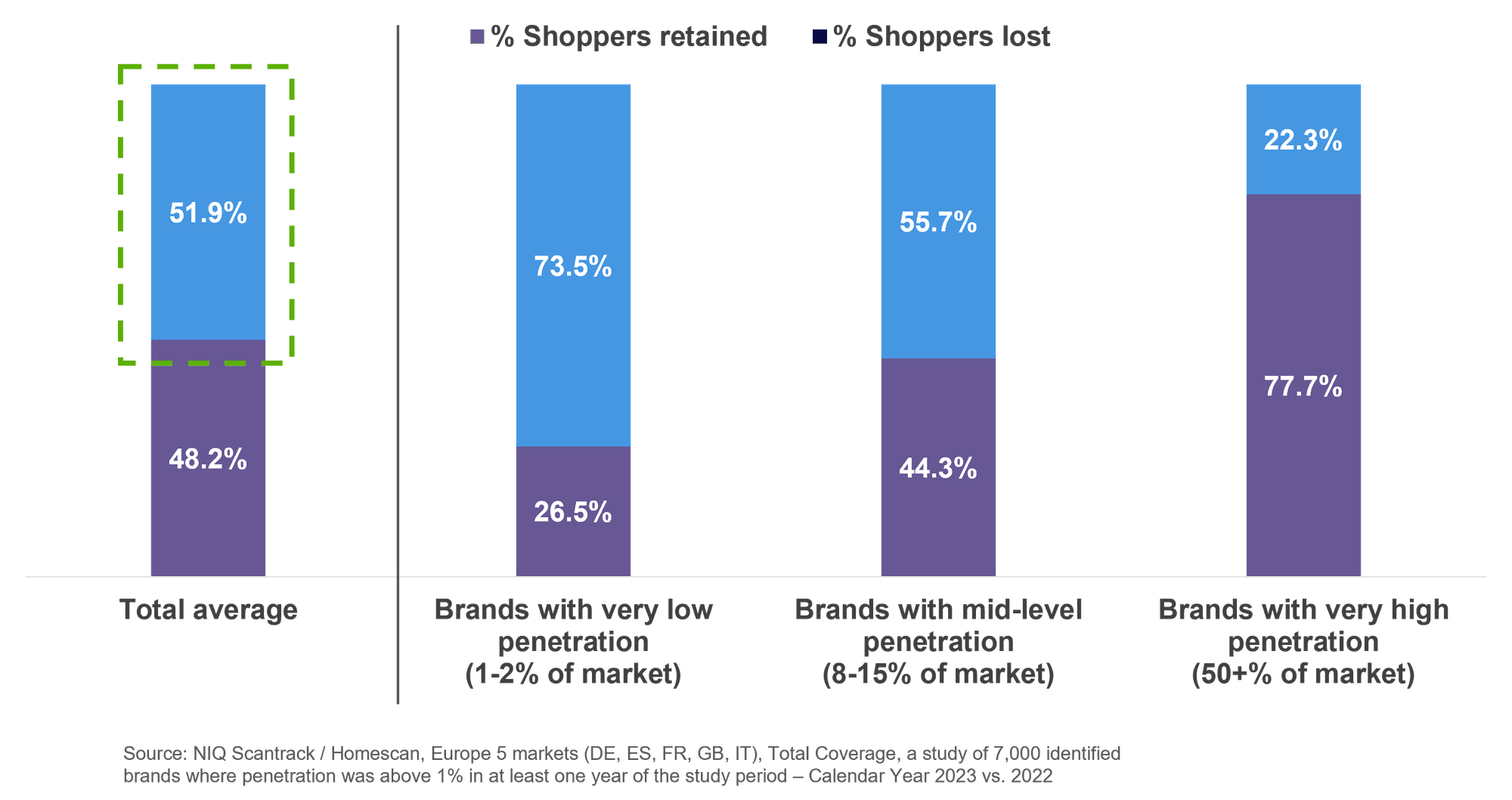

of a typical brand’s shoppers will not buy the brand again the next year.

(based on a European study of 7K identified brands)

All this talk of volume resiliency and the need for momentum-building brings us to a study conducted across five European markets to understand the keys to driving brand growth beyond inflation. Looking across 7,000 different brands, the study revealed the harsh reality that over half (52%) of a typical brand’s shoppers will not buy the same brand again the next year.

That’s an alarmingly high percentage of disloyal shoppers — and a stark reminder to companies that in today’s dynamic world, you must appeal to as many consumers as possible to survive and thrive over the long term.

of brands that saw declining volume, also lost penetration.

Penetration growth is

essential to volume growth.

of brands aren’t growing penetration.

More brands are losing shoppers than gaining them.

of a brand's shopper only buy once.

Many shoppers buy a brand just once, but every shot counts.

From this study, we can see a few additional reminders of how important penetration (and maximizing your pool of buyers) is to volume growth — and the challenges that brands face if scaling to the masses with the wrong strategy. Growth beyond inflation is possible. But it must be done with a full view into all available consumer targets (to know who you’re looking to engage) and with a deep understanding of how consumers of all financial circumstances will be spreading their spending across categories of interest.

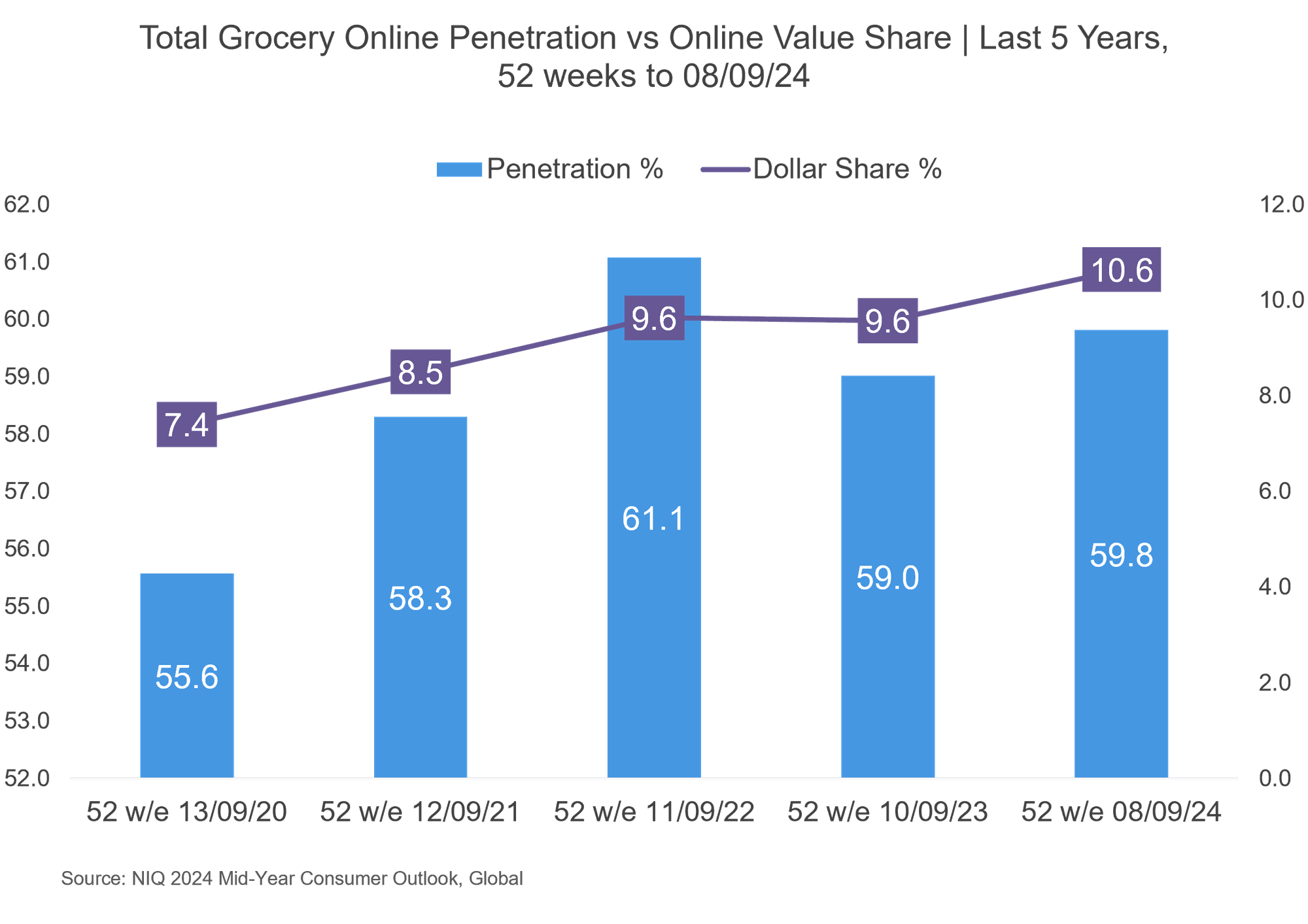

Online continues to gain share from Bricks & Mortar over the last 5 years, highlighting an opportunity for brands and retailers in this space. We know that covid accelerated the online development in Australia and the channel had plateaued post-covid, but now we see signs of online growth again, driven by a penetration recovery. The channel typically performs better among families and larger households as the convenience aspect of online is more appealing to them. Now it’s attracting a wider range of shoppers, including middle-aged and older singles and couples, highlighting its potential for expansion within these demographics.

Online is more consolidated within Families, but Independent Singles and Senior Couples are driving penetration growth in the last year.

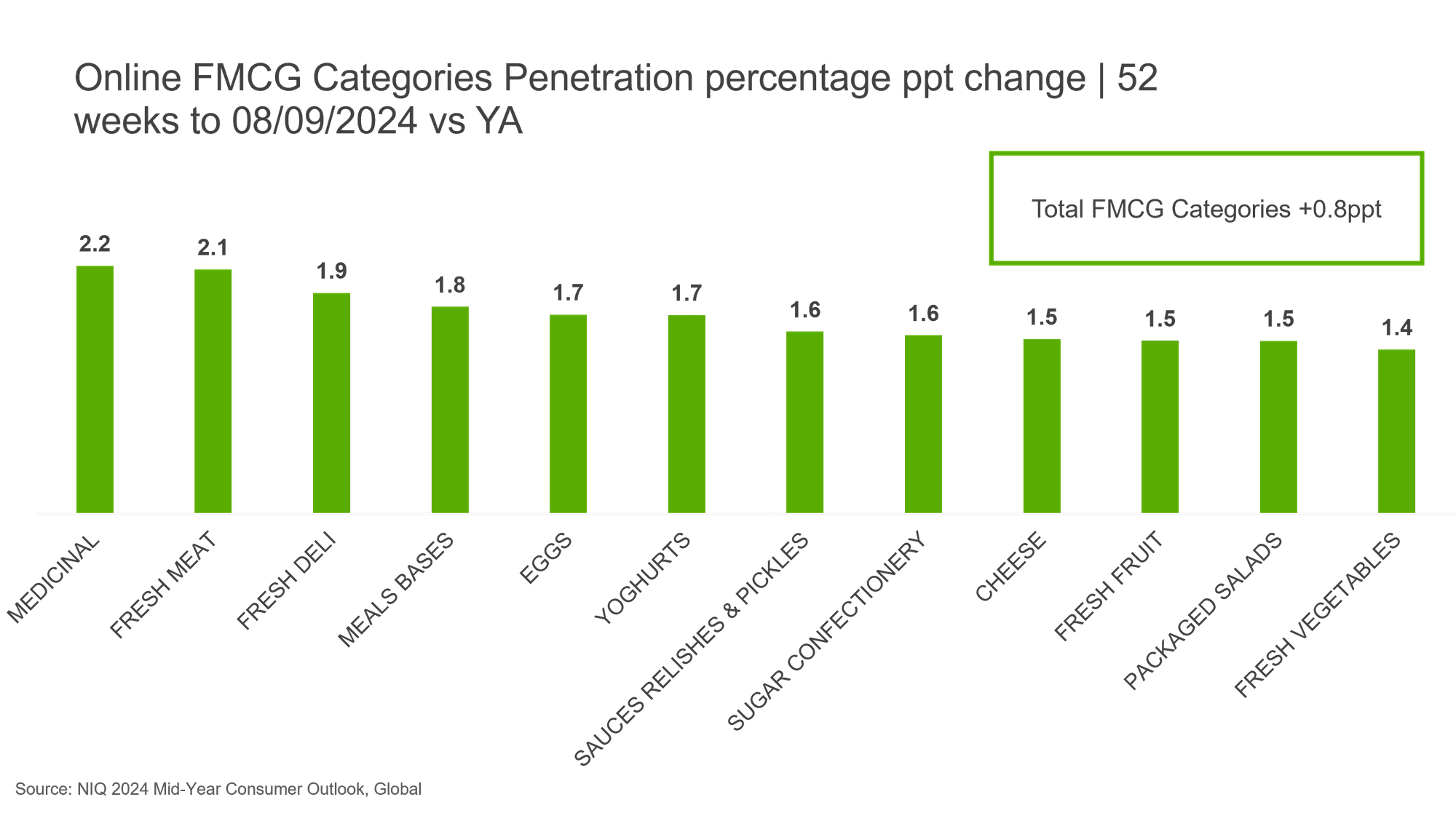

And some categories are developing their penetration strongly among the channel. It’s interesting to notice the gain of penetration for many Fresh categories, such as Meat, Deli, Fruits and Vegetables, suggesting that some of those barriers of Fresh products online are still been broken.

NIQ Discover connects businesses around the world to the latest cloud-based technology powered by the most accurate and trusted data in the industry to help them differentiate and win in a competitive environment.

Intuitive landing page for KPIs, alerts and quick access to your automatically refreshed scheduled reports

Powerful report and dashboard creation from building a basic table with your most granular data, to creating a sophisticated multiple sources report with tables & charts.

The best starting place to perform an analysis to answer top business questions for measurement and panel assets with best-in-class NIQ curated visuals, analysis & guided flow

make it easy to find your saved reports & personal charts and saved selections, and collaborate things that have been shared with you.

Industry-leading data paired with an intuitive, AI-powered experience to drive growth.

Discover more